来自:CFA > 2025 Level II > Portfolio Management > Learning Module 5 Measuring and Managing Market Risk 2025-05-28 13:22

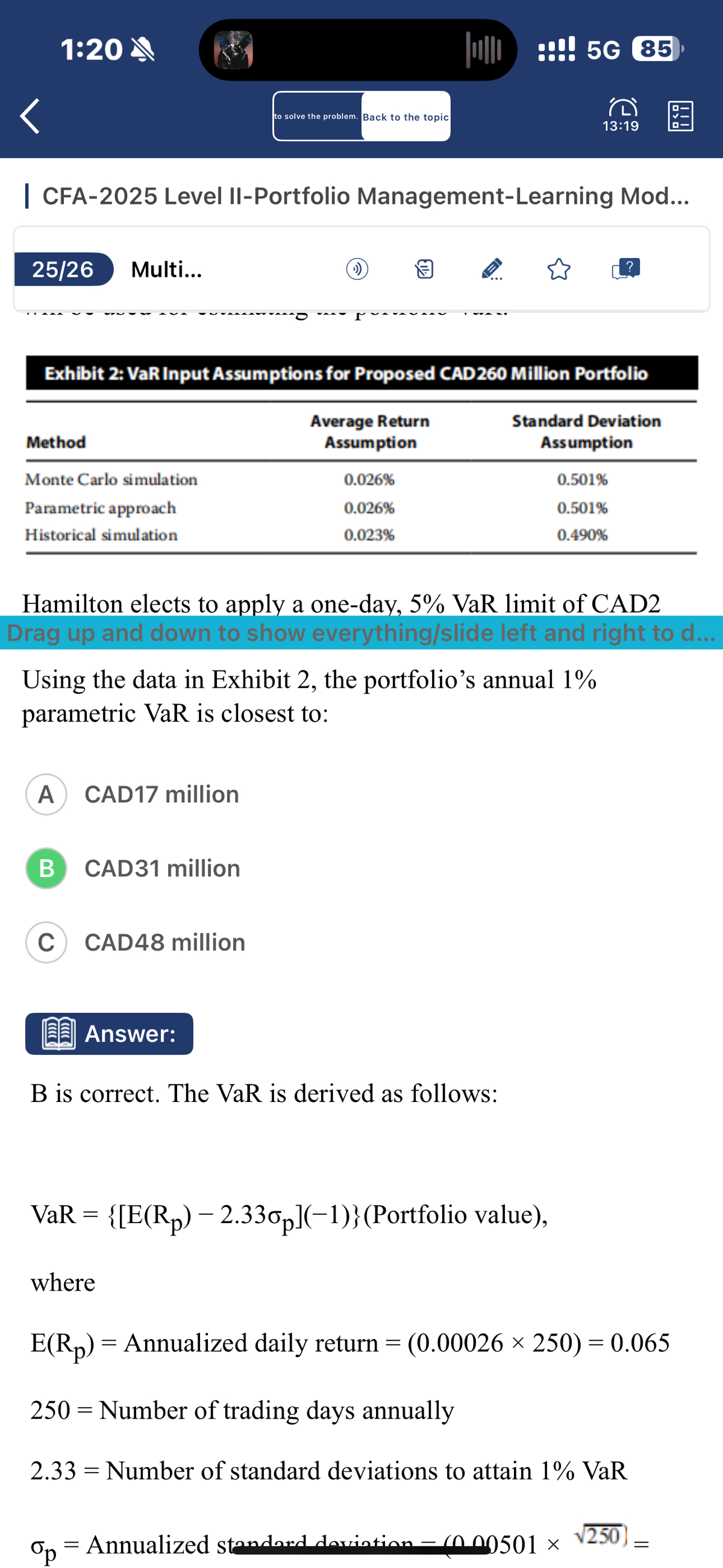

老師,這道題Exhibit 2有3個Method的數據,答案是直接用Average Return 2.6%作計算。不需要3個method取平均嗎?

查看更多

查看更多

172****0569

提问

9

上次登录

205天前